EU Data Center Sustainability Insights

Power consumption is rising rapidly, and data centers have become a source of national-level pressure.

The European market is entering a transition phase driven by policies and regulations.

Data centers must not only improve energy efficiency, disclose power consumption, and utilize waste heat, but also increase the use of renewable energy to align with the 2030 carbon neutrality targets.

For industry players, entering or expanding in the European market is no longer just a competition for land and capital — it has become a strategic test of compliance, transparency, and energy allocation.

1. According to a report by the European Commission’s Joint Research Centre (JRC), as of 2022,

According to a report by the European Commission’s Joint Research Centre (JRC), as of 2022, data centers in the EU consumed between 45 and 65 TWh of electricity annually, accounting for approximately 1.8–2.6% of the region’s total electricity consumption.

When including telecommunications networks, total electricity consumption across digital infrastructure reaches 70–95 TWh. By 2035, the total capacity of data centers is projected to grow to 26.6 GW , with electricity use reaching 236 TWh — accounting for approximately 5.7% of total consumption.

Image Source:ICIS

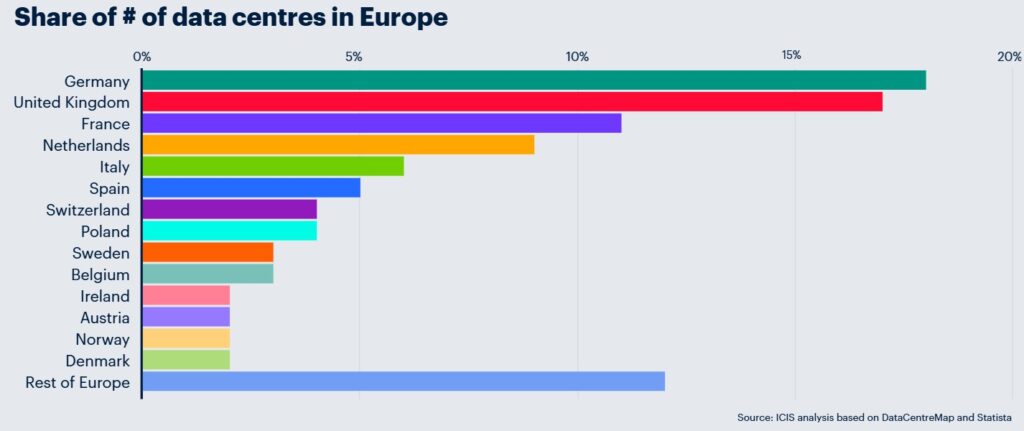

In addition to rapid growth in scale, the geographic concentration of data centers is also striking. Germany (around 450 sites), the United Kingdom (around 400), France, and the Netherlands (about 250 each) together account for more than half of all facilities in Europe. Centered around Frankfurt, London, Amsterdam, Paris, and Dublin (the FLAP-D markets), and extending to Milan, Madrid, and Berlin, these “core city clusters” represent over one-quarter of the entire European market.

At present, Europe’s data centers are highly concentrated in four major countries::

- Germany: approximately 450 facilities

- United Kingdom: approximately 400 facilities

- France and the Netherlands: approximately 250 facilities each

Together, they account for more than half of all data centers in Europe, with Frankfurt, London, Amsterdam, Paris, and Dublin (FLAP-D) forming the continent’s core region. per unit.

When expanded to include Milan, Madrid, and Berlin, these core cities together account for more than one-quarter of the entire European market.

In several countries, data centers have already become central topics in energy and policy discussions. For example:

- Ireland:electricity consumption accounts for a significant share of the country’s total power usage 18%

- The Netherlands:6%

- Luxembourg:5.5%

- Denmark:5%

2. Policy Shifts and Investment Momentum: From Regulatory Barriers to AI Factories

EU policies have shifted from encouragement to enforcement, integrating data centers into investment and procurement frameworks and creating mandatory market entry requirements.

- Disclosure obligations:The revised Energy Efficiency Directive requires data centers to disclose, every six months, their energy consumption, PUE, carbon emissions, and renewable-energy share, and to upload this data to the EU database.

- Equipment standards:Servers and storage equipment must meet the Ecodesign minimum energy efficiency requirements, while public procurement gives priority to high-efficiency, low-carbon equipment.

- Energy allocation:They must also increase the share of renewable energy and adopt waste heat recovery or water-cooling designs.

These three layers of pressure—disclosure, energy efficiency, and renewable energy—have become strict entry barriers to the European market. Projects that fail to meet them will struggle to gain investor confidence or policy support.

At the same time, the European Union is advancing these efforts through Horizon Europe、Digital Europe、InvestEU、Recovery and Resilience Facility funding instruments such as the Connecting Europe Facility (CEF) and the InvestEU program, accelerating the transformation of digital and energy infrastructure.

Particular focus on promoting AI Factory Project:

- Integration of data centers and AI supercomputing facilities

- Adoption of water-cooling systems and renewable energy frameworks

- With investments expected to exceed €20 billion by 2026

- Establish at least 15 AI factories and deploy 9 AI-optimized supercomputers

This signifies that data centers are no longer merely energy-saving facilities, but rather strategic pillars for Europe’s digital sovereignty and industrial advancement per unit.

3. Key Strategic Priorities for Enterprises Entering the European Market

For enterprises, entering or expanding in the European market is no longer merely a contest of investment scale and land cost, but rather a question of whether they can meet the new thresholds of energy and sustainability governance:

- Green power procurement capabilities and ESG performance: The European market requires data centers to gradually increase their share of renewable energy, meaning enterprises must have CPPA and robust carbon management capabilities; otherwise, they risk being excluded during bidding or investment attraction stages.

- Energy transparency and data disclosure: The energy disclosure system means that enterprises must have built-in real-time monitoring, data reporting, and compliance auditing processes. For companies accustomed to disclosing energy information only in financial reports, this represents a shift in their operating model and will also reshape the way internal IT, finance, and operations teams collaborate.

- Policy-driven funding and partnership opportunities: familiarity with programs such as Horizon Europe and InvestEU . Not only provides access to funding support but also enables participation in pilot projects, enhancing market visibility. For new entrants, this serves as a crucial shortcut to integrating into the local industry ecosystem.

For Taiwan, the technology industry and data center sector are growing rapidly, but if the country eventually adopts an EU-style energy disclosure and renewable energy compliance thresholds,it will bring several structural challenges:

- Insufficient supply of renewable energy:Currently, the green power market remains limited in scale, and a full mandate could lead to a supply–demand gap.

- Immature data governance frameworks:Most enterprises have yet to establish cross-departmental processes for energy monitoring and disclosure.

- Intensifying international competitive pressure:Failing to align early with EU requirements may constrain their competitiveness in the international market.

Further Reading|EU Data Center Sustainability (Part 2):Data Center Transformation Series (Part II): The Renewable Energy Race Behind Taiwan’s Tech Industry

References:

Data Center Regulation Trends to Watch in 2025: https://www.datacenterknowledge.com/regulations/data-center-regulation-trends-to-watch-in-2025

ICIS:https://www.icis.com/explore/resources/data-centres-hungry-for-power/

Leave a Reply